Satinder Pal Singh

Contact Info:

About

Languages:

Mortgage Services

New to Canada

First Time Home Buyers

Explore Our Services

Preview Our Rates

Access all your mortgage options with just one application. Preview today's rates first:

Blog

Canada's Economic Outlook for 2026: What Homeowners and Buyers Should Know

January 12, 2026

Canada's Economic Outlook for 2026: What Homeowners and Buyers Should Know

Economic Growth Projection

Canada's economy projected to grow 1.4% to 1.5% in 2026.

Growth rate below historical trends.

Economic expansion limited by trade tensions and structural challenges.

Housing Market Conditions

Price Moderation Expected

- House prices showing moderation across Canada

- Ontario and British Columbia experiencing significant corrections

- Real estate volatility decreasing from previous years

- Market stabilization creating opportunities for buyers

Edmonton Market Implications

Edmonton housing market positioned for steady activity.

Alberta economic conditions more stable than Ontario counterparts.

Regional advantages in affordability compared to Vancouver and Toronto markets.

Interest Rate Environment

Bank of Canada Policy Changes

Rate cuts totaling 275 basis points since 2024.

Four additional cuts implemented in 2025.

Monetary policy easing continues into 2026.

Mortgage Relief Impact

- Refinancing opportunities increased for existing homeowners

- Variable rate mortgage holders experiencing payment reductions

- Fixed rate renewal options improved from 2024-2025 highs

- Debt servicing ratios becoming more manageable

Economic Headwinds

Trade Relations

U.S. trade disputes affecting Ontario and Quebec economies.

CUSMA renegotiation scheduled for July 2026.

Trade uncertainty impacting business investment decisions.

Employment Conditions

- Business hiring expected to slow in first half 2026

- Job security concerns affecting buyer confidence

- Consumer spending growth limited despite rate relief

- Household purchasing power under pressure

Population Dynamics

Immigration Impact

Population growth flattening in 2026.

Immigration volumes declining from 2023-2024 peaks.

Housing demand pressure reducing accordingly.

Labor Market Adjustments

Unemployment rates expected to decline.

Labor demand reduction offsetting immigration decreases.

Per-capita GDP improvement anticipated after three-year decline.

Mortgage Market Opportunities

First-Time Buyers

- Improved affordability from price moderation

- Lower carrying costs from rate reductions

- Enhanced qualification prospects with stable employment

- Regional advantages in Edmonton market

Existing Homeowners

Renewal opportunities at favorable rates.

Refinancing options for debt consolidation.

Home equity access improved with rate environment.

Regional Economic Factors

Alberta Advantages

Energy sector providing economic stability.

Provincial fiscal position stronger than eastern counterparts.

Interprovincial migration supporting housing demand.

Edmonton Specific Conditions

- Balanced housing supply and demand

- Government sector employment stability

- Infrastructure investment supporting growth

- University and health sector anchoring economy

Market Timing Considerations

Short-Term Outlook

First half 2026 showing cautious market conditions.

Economic uncertainty affecting buyer and seller decisions.

Rate environment favorable for qualified borrowers.

Long-Term Perspective

Second half 2026 dependent on trade resolution.

Election outcomes affecting economic confidence.

Market fundamentals supporting gradual improvement.

Mortgage Strategy Implications

Rate Environment

- Variable rate mortgages showing advantage

- Fixed rate terms offering stability

- Hybrid products balancing risk and opportunity

- Renewal timing critical for optimization

Qualification Standards

Stress test requirements unchanged.

Income verification maintaining current standards.

Down payment requirements stable.

Alternative lending options available for unique situations.

Professional Guidance Requirements

Market complexity requiring expert navigation.

Rate comparison essential for optimal outcomes.

Timing coordination critical for buyers and refinancers.

Mortgage services providing comprehensive support.

Economic Indicators Monitoring

Key Metrics

- GDP growth quarterly reports

- Employment statistics monthly releases

- Inflation data Bank of Canada tracking

- Housing starts and sales activity

Decision Triggers

Trade agreement resolution timing.

Federal election outcome impacts.

Provincial policy changes affecting real estate.

Bank of Canada policy announcement schedule.

Risk Assessment

Downside Scenarios

Trade dispute escalation.

Economic growth below projections.

Employment conditions deteriorating faster than expected.

Upside Potential

Trade resolution boosting confidence.

Immigration policy supporting demand.

Energy sector performance exceeding expectations.

Action Items for 2026

Current Homeowners

Review renewal options early.

Assess refinancing opportunities.

Monitor rate environment developments.

Prospective Buyers

Evaluate pre-approval timing.

Research Edmonton market conditions.

Affordability calculator analysis recommended.

Real Estate Professionals

Client education on economic factors.

Market timing strategy development.

Professional collaboration for optimal outcomes.

Economic outlook requiring careful navigation. Professional mortgage guidance essential for optimal 2026 market positioning.

Please note: Economic projections are based on the latest available data and expert forecasts, but conditions can change quickly. This post is for informational purposes only and shouldn’t be considered financial advice. For personal guidance, always consult a qualified professional.

How a $10,000 Down Payment Turned Into $100K Profit: Real Investor Success Story in Scarborough, ON

November 20, 2025

How a $10,000 Down Payment Turned Into $100K Profit: Real Investor Success Story in Scarborough, ON

Case Study Overview

Property investment completed in Scarborough, Ontario. Client secured short-term financing for renovation and resale project.

Key Metrics:

- Mortgage Amount: $627,000

- Down Payment: $10,000

- Position: First mortgage

- LTV: 66.21% (based on after-repair value)

- Interest Rate: 17.25%

- Timeline: 3.5 months

- Net Profit: $100,000

Project Structure

Financing Terms:

- First mortgage position

- Short-term private lending

- Interest-only payments during renovation

- Exit strategy: Property sale upon completion

Property Details:

- Location: Scarborough, Ontario

- Purpose: Renovation and resale

- After-repair value calculation: LTV 66.21%

Down Payment Strategy

Client invested $10,000 total for:

- Property acquisition

- Renovation costs

- Carrying costs during project

Capital Requirements:

- Down payment: $10,000

- Mortgage funding: $627,000

- Total project value supported by after-repair value assessment

Timeline Breakdown

Month 1:

- Property acquisition completed

- Renovation planning finalized

- Construction commenced

Month 2-3:

- Active renovation period

- Property improvements executed

- Market preparation initiated

Month 3.5:

- Project completion

- Property listing and sale

- Mortgage discharge

Financial Analysis

Revenue Structure:

- Sale price achieved target after-repair value

- Gross profit generated: $100,000

- Return on invested capital: 1000%

Cost Components:

- Interest payments at 17.25%

- Renovation expenses

- Carrying costs

- Transaction fees

Risk Management

LTV Calculation:

- Based on after-repair value: 66.21%

- Conservative valuation approach

- Market analysis verification

Exit Strategy Elements:

- Clear resale timeline

- Market demand assessment

- Price point validation

Low Down Payment Benefits

Capital Efficiency:

- Minimal upfront investment required

- Preserved liquidity for additional opportunities

- Leveraged financing structure

Portfolio Flexibility:

- Multiple project capability

- Risk distribution across investments

- Cash flow management optimization

Alternative Lending Structure

Private Mortgage Features:

- Speed of approval and funding

- Asset-based underwriting

- Flexible terms for renovation projects

- Short-term commitment alignment

Comparison to Traditional Financing:

- Conventional mortgages: Lengthy approval process

- Private lending: Project-specific evaluation

- Interest rate reflection of risk and timeline

Scarborough Market Factors

Location Advantages:

- Established residential market

- Renovation opportunity availability

- Buyer demand consistency

- Price appreciation potential

Market Timing:

- Project completion aligned with market conditions

- Seasonal considerations addressed

- Buyer activity optimization

Investment Strategy Implementation

Project Selection Criteria:

- After-repair value calculation accuracy

- Renovation scope definition

- Timeline feasibility assessment

- Market demand validation

Execution Requirements:

- Contractor coordination

- Budget management

- Timeline adherence

- Quality control maintenance

Financing Application Process

Documentation Requirements:

- Property assessment

- Renovation plans

- Budget projections

- Exit strategy documentation

Approval Factors:

- After-repair value verification

- Client experience evaluation

- Project viability assessment

- Risk analysis completion

Disclaimers and Considerations

Interest Rate Variables:Interest rates and fees determined on deal-by-deal basis. Multiple factors influence rate determination. Contact for current rate information.

Profit Considerations:Net profits not guaranteed. Results vary depending on project specifics, market conditions, and execution quality.

Risk Factors:

- Market fluctuation impact

- Renovation cost overruns

- Timeline extension possibilities

- Sale price variations

Alternative Lending Access

Private mortgage options available for qualified borrowers. Project-specific evaluation process. Professional consultation recommended for investment planning.

Service Categories:

- Short-term renovation financing

- Bridge loan solutions

- Investment property funding

- Alternative qualification criteria

For investment financing consultation: Contact mortgage services

Additional Resources:

- Alternative lender information: Bad credit solutions

- First-time buyer guidance: Home buying guide

Project Success Factors

Critical Elements:

- Accurate after-repair value assessment

- Realistic renovation timeline

- Market analysis precision

- Professional contractor selection

Outcome Drivers:

- Project completion within budget

- Timeline adherence

- Market timing optimization

- Quality renovation execution

This case study demonstrates successful implementation of low down payment investment strategy using private mortgage financing for renovation and resale project in Scarborough, Ontario market.

Struggling with Bad Credit? 7 Alternative Lender Secrets That Could Get You Approved in Alberta

October 31, 2025

Struggling with Bad Credit? 7 Alternative Lender Secrets That Could Get You Approved in Alberta

Alternative lenders in Alberta operate under different approval criteria than traditional banks. Bad credit borrowers access financing through specific lender categories and application strategies.

Secret 1: Income-Based Approval Systems Replace Credit Score Requirements

Payday lenders base approval decisions on income verification rather than credit scores. Most payday lenders eliminate credit checks entirely from their approval process.

Income-Focused Lenders:

- Payday loan providers

- Cash advance services

- Short-term installment lenders

- Online alternative lenders

Income requirements typically range from $1,000 to $2,000 monthly. Employment verification occurs through pay stubs or bank statements. Self-employed applicants provide income documentation through tax returns or bank deposit records.

Alternative lenders evaluate debt-to-income ratios instead of credit history patterns. Employment stability carries more weight than credit score numbers in approval algorithms.

Secret 2: Regulatory Changes Create Lower Cost Options

Alberta implemented 35% APR maximum rates for personal loans effective January 1, 2025. Previous maximum rates reached 47% APR for alternative lenders.

Rate Structure Changes:

- Personal loans: 35% APR maximum

- Payday loans: $14 per $100 borrowed

- Cash advance apps: Zero interest options available

- Secured loans: Lower rates due to collateral backing

Licensed lenders must comply with provincial rate caps. Unlicensed operators charge higher rates outside regulatory framework.

Secret 3: Secured Loan Approval Rates Exceed 90%

Collateral-backed loans generate highest approval rates for bad credit applicants. Lenders accept various asset types as security for loan amounts.

Accepted Collateral Types:

- Vehicle titles

- Real estate equity

- Investment accounts

- Savings deposits

- Equipment and machinery

Loan amounts range from $500 to $50,000 based on collateral value. Interest rates decrease with higher-value security assets.

Asset appraisal determines maximum loan amounts. Borrowers retain asset use during loan term in most cases.

Secret 4: Cash Advance Apps Eliminate Traditional Loan Costs

Mobile applications provide $30 to $500 advances without mandatory fees or interest charges. Three-day standard delivery includes no costs to borrowers.

Cash Advance Features:

- No credit checks required

- Income verification through bank connections

- Optional instant funding with fees

- Monthly subscription models available

- Automatic repayment scheduling

Apps generate revenue through optional expedited transfer fees and subscription services rather than loan interest.

Secret 5: Co-Signer Relationships Unlock Traditional Loan Products

Co-signers with good credit expand loan options beyond alternative lender products. Traditional banks approve applications with qualified co-signers regardless of primary borrower credit scores.

Co-Signer Requirements:

- Credit score above 650

- Stable employment history

- Debt-to-income ratio below 40%

- Legal responsibility for loan payments

Co-signed loans access lower interest rates than alternative lender products. Loan amounts increase based on co-signer income and credit profile.

Secret 6: Vehicle Financing Operates Under Different Approval Standards

Auto loans utilize vehicle collateral to reduce lender risk. Approval rates exceed unsecured personal loan approval rates for identical credit profiles.

Vehicle Loan Advantages:

- Lower interest rates than personal loans

- Extended repayment terms available

- Higher loan amounts approved

- Less stringent credit requirements

Used vehicle financing accepts credit scores below 500 in many cases. New vehicle loans require higher credit thresholds but offer better terms than alternative lenders.

Dealer financing partnerships connect bad credit buyers with specialized auto lenders. Independent financing comparison improves rate outcomes.

Secret 7: Mortgage Brokers Access Private and B-Lender Networks

Mortgage brokers maintain relationships with private lenders and B-lenders specializing in poor credit home financing. Traditional bank rejection does not eliminate home purchase options.

Alternative Mortgage Sources:

- Private lenders with flexible criteria

- B-lenders accepting credit scores below 580

- Some lenders with no minimum credit requirements

- Asset-based lending programs

Private mortgage rates range from 6% to 12% annually. B-lender rates typically fall between traditional bank rates and private lender rates.

Down payment requirements increase with lower credit scores. Alternative mortgage terms may include shorter amortization periods or higher down payment percentages.

Application Strategy Framework

Documentation Requirements:

- Recent pay stubs or income statements

- Bank statements from previous 3 months

- Government-issued identification

- Proof of address documentation

- Employment verification letters

Pre-Application Steps:

- Calculate accurate debt-to-income ratios

- Gather required documentation

- Research licensed lender options

- Compare rate structures across lender types

Application Timing Considerations:

- Submit applications during business hours

- Avoid multiple applications within short timeframes

- Allow 24-48 hours for initial approval decisions

- Prepare for potential documentation requests

Risk Management and Cost Analysis

Alternative lending carries higher costs than traditional banking products. Borrowers must evaluate total loan costs against financing needs and repayment capacity.

Cost Comparison Framework:

- Calculate total interest paid over loan term

- Include all fees in cost analysis

- Compare APR rates across lender options

- Evaluate early payment penalty structures

Emergency financing situations may justify higher costs. Non-emergency borrowing benefits from extended comparison shopping and rate negotiation.

Financial Counseling Resources:

- Credit Counselling Canada: 1-866-398-5999

- Non-profit credit counseling services

- Alberta government financial literacy programs

Licensed lender verification prevents predatory lending exposure. Provincial licensing databases confirm lender legitimacy before application submission.

Credit Rebuilding Through Alternative Lending

Some alternative lenders report payment history to credit bureaus. On-time payments improve credit scores over loan terms.

Credit Building Lenders:

- Installment loan providers

- Secured credit card programs

- Credit builder loan products

- Rent reporting services

Payment reporting policies vary by lender. Confirm credit bureau reporting before loan acceptance to maximize credit improvement opportunities.

Regular payment history creates positive credit references for future traditional lending applications. Alternative lending serves as bridge financing while rebuilding creditworthiness.

Alternative lender approval rates exceed traditional bank approval rates for bad credit applicants. Income verification, collateral security, and co-signer relationships provide multiple approval pathways outside conventional banking systems.

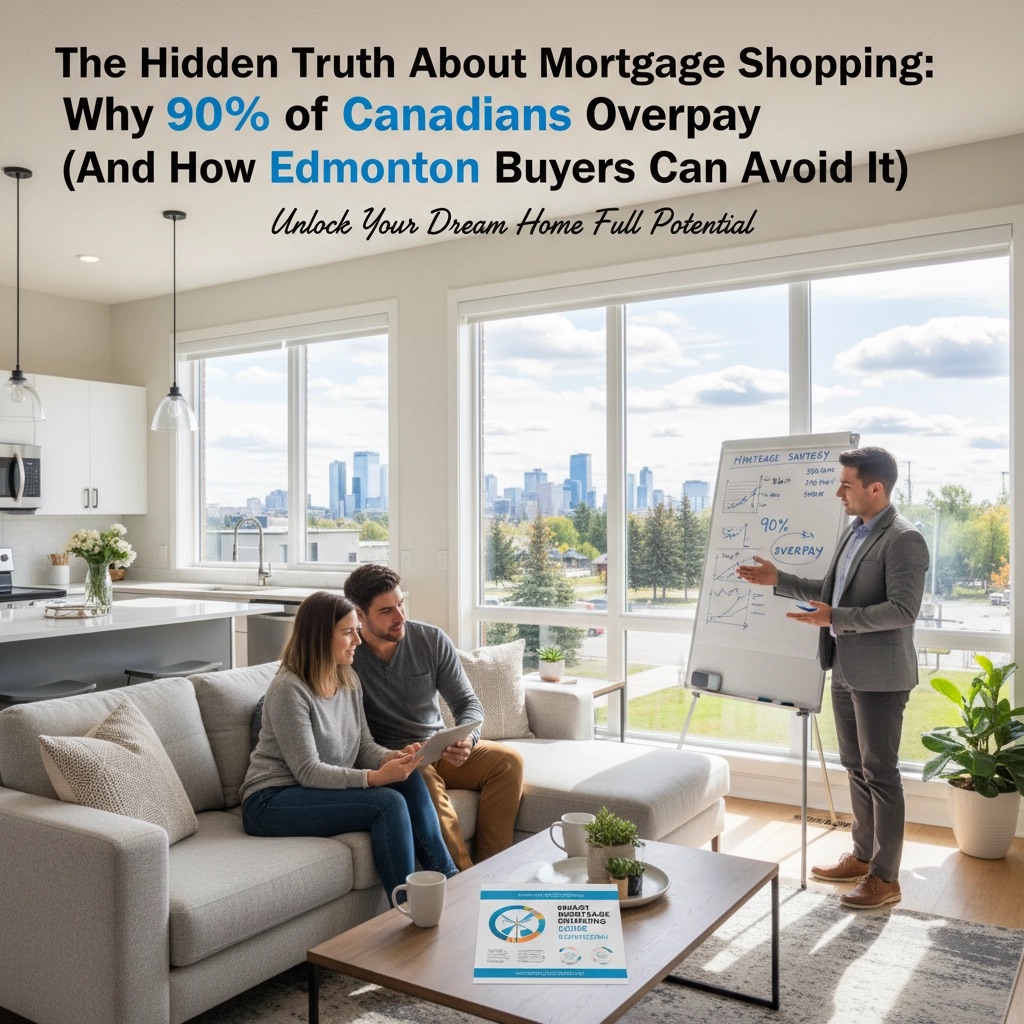

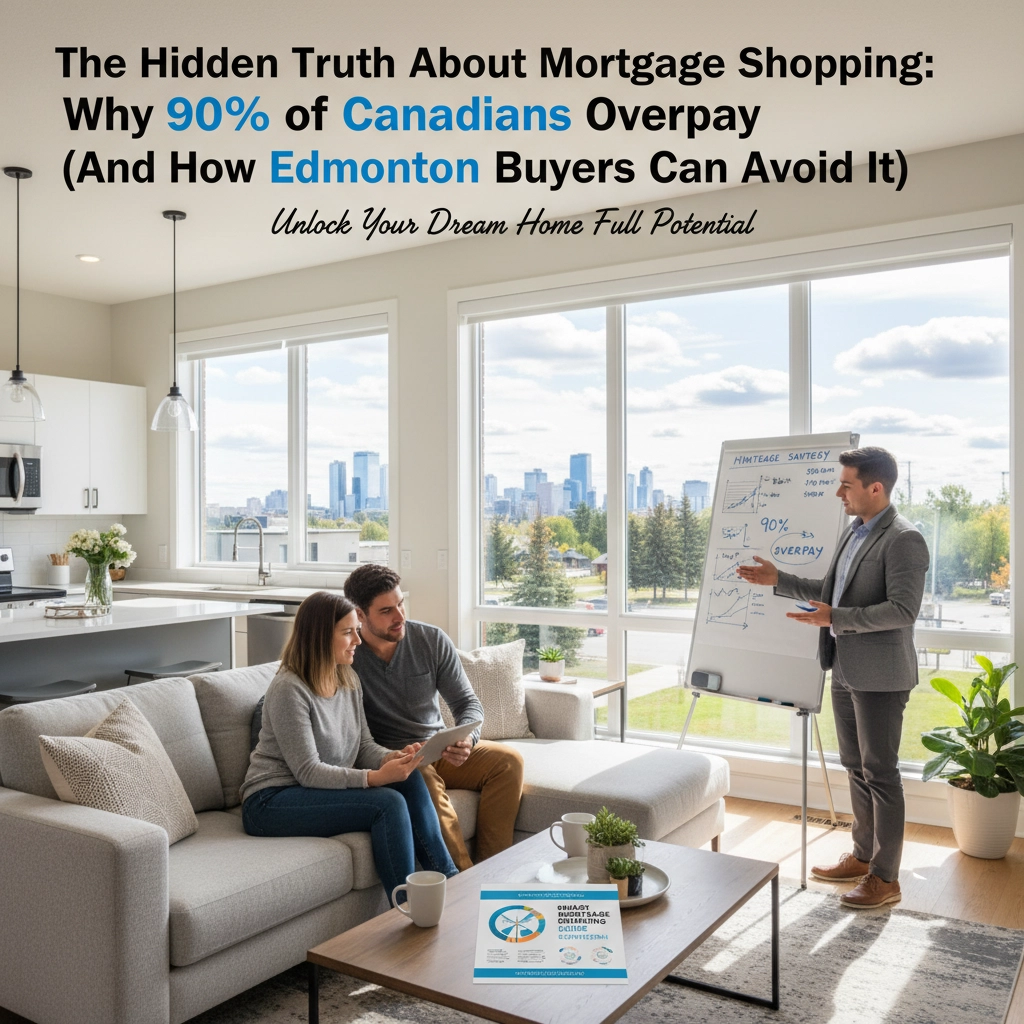

The Hidden Truth About Mortgage Shopping: Why 90% of Canadians Overpay (And How Edmonton Buyers Can Avoid It)

October 22, 2025

The Hidden Truth About Mortgage Shopping: Why 90% of Canadians Overpay (And How Edmonton Buyers Can Avoid It)

The Real Numbers

Data shows 43% of mortgage holders obtained only one quote before securing their mortgage rate. This statistic represents significant financial loss potential.

Cost Analysis:

- 0.1% rate difference = hundreds saved annually

- $400,000 mortgage example = tens of thousands over 25 years

- Single quote approach = missed savings opportunities

Current Market Conditions

Payment Pressure Statistics

Financial Strain Data:

- Two-thirds of mortgage holders report difficulty meeting commitments

- One-third can meet payments without difficulty

- 22.2 percentage point decrease in payment comfort since August 2020

Renewal Timeline

Upcoming Renewals:

- 60% of outstanding mortgages renew by end of 2026

- 40% expected to renew at higher rates

- 74% of holders face renewal within three years

Payment Increase Projections:

- 2025 renewals: 10% higher monthly payments average

- 2026 renewals: 6% higher monthly payments average

- 15% of renewals: 10-20% payment increases

- 25% of renewals: 20%+ payment increases

Why Shopping Stops at One Quote

Common Factors

Misconceptions:

- First offer acceptance standard practice

- Renewal automatic process assumption

- Rate focus over complete package evaluation

Process Barriers:

- Time constraints

- Application complexity

- Limited lender awareness

Edmonton Market Specifics

Local Considerations

Edmonton Factors:

- Competitive real estate environment

- Regional lender variations

- Market timing implications

Available Options:

- Traditional banks

- Credit unions

- Online lenders

- Mortgage brokers

Comparison Shopping Framework

Lender Categories

Traditional Banks:

- Posted rates

- Negotiation potential

- Package deals

Credit Unions:

- Member benefits

- Local market knowledge

- Competitive rates

Online Lenders:

- Lower overhead costs

- Streamlined processes

- Rate competitiveness

Mortgage Brokers:

- Multiple lender access

- Rate comparison services

- Professional guidance

Quote Collection Process

Minimum Requirements:

- Three lender quotes minimum

- Five quotes recommended

- Same qualification parameters

- Identical mortgage terms

Documentation Consistency:

- Income verification

- Down payment amount

- Property details

- Credit score range

Rate Impact Analysis

Financial Calculations

Example Scenarios:

$300,000 Mortgage:

- 0.1% difference = $150 annual savings

- 25-year term = $3,750 total savings

$500,000 Mortgage:

- 0.1% difference = $250 annual savings

- 25-year term = $6,250 total savings

$700,000 Mortgage:

- 0.1% difference = $350 annual savings

- 25-year term = $8,750 total savings

Compound Savings Impact

Long-term Benefits:

- Principal reduction acceleration

- Interest payment minimization

- Equity building enhancement

Beyond Rate Comparison

Complete Package Evaluation

Rate Components:

- Posted rate

- Negotiated rate

- Variable vs fixed options

Fee Structure:

- Application fees

- Appraisal costs

- Legal fees

- Discharge penalties

Terms and Conditions:

- Prepayment privileges

- Payment frequency options

- Renewal conditions

- Portability features

Prepayment Options

Standard Features:

- 10-20% annual prepayment allowance

- Double-up payment options

- Lump sum payment dates

Strategic Applications:

- Principal reduction acceleration

- Interest savings maximization

- Mortgage term shortening

Professional Guidance Benefits

Mortgage Broker Advantages

Access Benefits:

- Multiple lender networks

- Wholesale rate access

- Product variety exposure

Service Components:

- Application management

- Documentation coordination

- Renewal assistance

- Refinancing options

Cost Structure:

- Lender compensation model

- No direct client fees typically

- Ongoing relationship benefits

Renewal Strategy

Automatic Renewal Risks

Default Process Problems:

- Current lender rate acceptance

- Limited negotiation opportunity

- Market rate comparison absence

Proactive Approach

Timeline Management:

- 120 days pre-renewal preparation

- Rate lock timing optimization

- Alternative lender exploration

Negotiation Points:

- Current relationship value

- Payment history leverage

- Market rate benchmarking

Edmonton-Specific Resources

Local Market Support

Available Services:

- Regional mortgage brokers

- Local credit union options

- Edmonton-focused lenders

Market Knowledge:

- Neighborhood pricing trends

- Property value assessments

- Regional economic factors

Implementation Steps

Phase 1: Preparation

Documentation Assembly:

- Income statements

- Credit report review

- Down payment verification

- Debt obligation summary

Phase 2: Quote Collection

Systematic Approach:

- Lender list creation

- Application timing coordination

- Rate comparison tracking

- Terms documentation

Phase 3: Analysis

Evaluation Framework:

- Total cost calculations

- Feature comparison matrix

- Professional consultation

- Decision timeline establishment

Phase 4: Selection

Final Assessment:

- Rate confirmation

- Terms finalization

- Application submission

- Timeline management

Market Trends Impact

Fixed vs Variable Preferences

Current Statistics:

- 68% choose fixed-rate mortgages

- Variable-rate holders make extra payments twice as frequently

- Payment stability priority increase

Renovation and Equity Access

Usage Patterns:

- 70% of homeowners renovate or plan renovations

- Rental income necessity for housing costs

- Refinancing for debt consolidation

Warning Signs

Overpayment Indicators

Process Red Flags:

- Single quote acceptance

- Automatic renewal selection

- Fee structure ignorance

- Prepayment option neglect

Financial Symptoms:

- Payment strain increase

- Refinancing frequency

- Debt consolidation requirements

The mortgage shopping landscape requires systematic approach. Rate differences accumulate substantial savings over mortgage terms. Edmonton buyers access multiple lender options through proper comparison processes.

Professional guidance provides lender network access and negotiation support. Renewal periods offer optimization opportunities requiring proactive management rather than automatic acceptance.

Market conditions favor prepared borrowers who understand complete package evaluation beyond rate focus alone.

Stay Connected

Subscribe to our Newsletter and you'll stay up to date on rates that help you save thousands in interest.